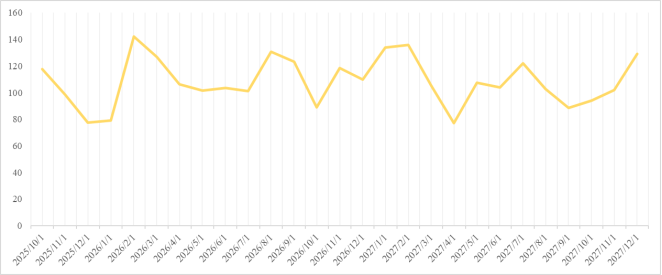

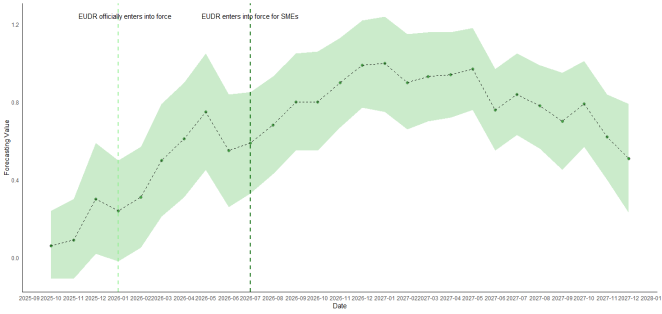

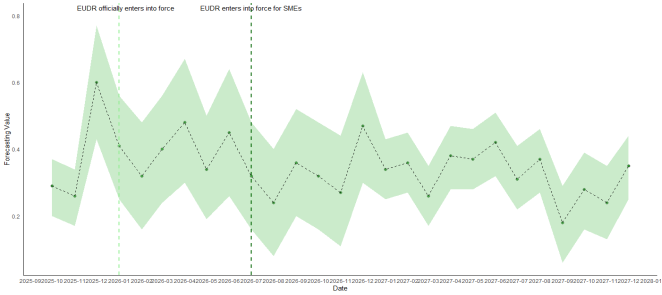

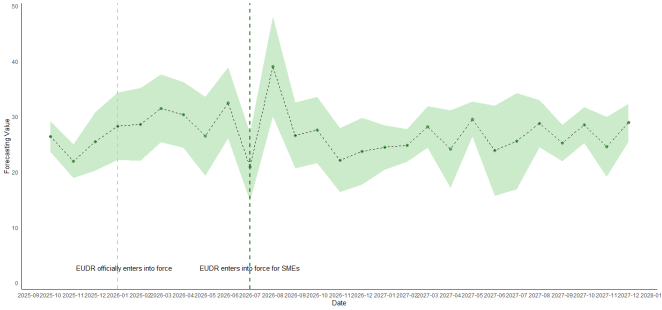

This study provides a comprehensive, quantitative forecast of the dynamic impact of the European Union Deforestation Regulation (EUDR) on forest product exports from nine major Asia-Pacific economies to the EU market. To address the complexity of this policy shock, we develop a novel two-stage forecasting framework that integrates LASSO regression for high-dimensional variable selection with OLS modeling. This approach generates dynamic monthly projections from October 2025 to December 2027, simulating the policy’s effect by combining a historical proxy from the European Union Timber Regulation (EUTR) with a calibrated “intensity multiplier” based on the EUDR country-risk classification. Our projections reveal a distinct multi-phase adjustment process across the region: an immediate, sharp contraction in Q4 2025, followed by a period of significant volatility and supply chain disruption throughout 2026, and an uneven recovery in 2027. The findings underscore substantial heterogeneity in impacts driven by the EUDR risk-based framework. Standard-risk countries, such as Indonesia and Malaysia, are projected to face severe volatility and suppressed growth trajectories, with Malaysia’s exports showing particular vulnerability. In contrast, some smaller, low-risk nations like the Philippines may capitalize on a substitution effect, gaining market share as larger suppliers struggle with compliance. The study concludes that the EUDR acts as a powerful disruptive force, reshaping competitive dynamics and necessitating urgent policy responses, including enhanced traceability infrastructure and strategic market diversification, for Asia-Pacific exporters.

| Published in | American Journal of Environmental and Resource Economics (Volume 10, Issue 4) |

| DOI | 10.11648/j.ajere.20251004.14 |

| Page(s) | 149-160 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

EU Deforestation Regulation (EUDR), Forest Product Trade, Asia-Pacific, Time-series Forecasting, LASSO

Country | Philippines | Japan | Korea | Singapore | New Zealand | Indonesia | Vietnam | Thailand | Malaysia |

|---|---|---|---|---|---|---|---|---|---|

Unit (Million) | USD | USD | USD | USD | USD | USD | USD | Thai Baht | Ringgit |

Mean | 0.5327 | 0.3470 | 0.5927 | 0.5842 | 3.3493 | 26.6307 | 62.7781 | 126.5784 | 54.7765 |

Median | 0.4502 | 0.3308 | 0.5400 | 0.5185 | 3.2502 | 26.7732 | 57.5779 | 120.1666 | 53.6988 |

Standard Deviation | 0.3490 | 0.1382 | 0.2265 | 0.4326 | 1.6299 | 5.7671 | 18.1886 | 52.0030 | 13.1694 |

Variance | 0.1218 | 0.0191 | 0.0513 | 0.1871 | 2.6566 | 33.2592 | 330.8267 | 2704.3084 | 173.4340 |

CV | 0.3490 | 0.1382 | 0.2265 | 0.4326 | 1.6299 | 5.7671 | 18.1886 | 52.0030 | 13.1694 |

Variable Name | Unit | Resource | Mean | Median | Standard Deviation | Variance | CV |

|---|---|---|---|---|---|---|---|

EU 27 Furniture Import Volume | Billion EUR | CEIC | 1.43 | 1.36 | 0.43 | 0.18 | 0.43 |

EU Total Import Volume | Billion EUR | CEIC | 167.45 | 152.57 | 37.88 | 1435.25 | 37.88 |

China’s Export Volume of Wood Products for Household or Decoration Use (Month-over-Month Growth Rate) | % | CEIC | 0.00 | 0.00 | 0.56 | 0.31 | 0.56 |

EUR/RMB | EUR/RMB | CEIC | 7.65 | 7.72 | 0.41 | 0.17 | 0.41 |

USD/RMB | USD/RMB | CEIC | 6.66 | 6.69 | 0.36 | 0.13 | 0.36 |

China CPI | (2015=100) | CEIC | 107.28 | 107.70 | 6.64 | 44.07 | 6.64 |

Malaysia (Plywood & Veneer) Production Volume | Cubic Meters | Department of Statistics Malaysia | 315322.06 | 288486.50 | 79401.54 | 6304604414.15 | 79401.54 |

Malaysia Unemployment Rate | % | Department of Statistics Malaysia | 3.51 | 3.40 | 0.55 | 0.30 | 0.55 |

Malaysia’s Total Export Volume to the EU | Million Malaysian Ringgit | Department of Statistics Malaysia | 7498.27 | 7282.15 | 1868.68 | 3491976.12 | 1868.68 |

USD/MYR | USD/MYR | Central Bank of Malaysia | 4.08 | 4.17 | 0.45 | 0.20 | 0.45 |

Malaysia CPI | (2010=100) | Department of Statistics Malaysia | 120.45 | 120.80 | 7.79 | 60.63 | 7.79 |

Thailand CPI | (2023=100) | Office of Trade Policy and Strategy | 93.69 | 92.20 | 3.93 | 15.41 | 3.93 |

Thailand’s Total Export Volume to the EU | Million Thai Baht | Ministry of Commerce | 65899.07 | 65517.85 | 8822.00 | 77827752.84 | 8822.00 |

Thailand Loan Interest Rate | Annual Interest Rate % | Bank of Thailand | 21.27 | 22.11 | 1.28 | 1.63 | 1.28 |

USD/THB | USD/THB | Bank of Thailand | 33.23 | 33.07 | 1.93 | 3.71 | 1.93 |

USD/VND | USD/VND | State Bank of Vietnam | 22677.52 | 22947.50 | 1032.04 | 1065098.59 | 1032.04 |

Brent Crude Oil Price | USD/Barrel | CEIC | 72.49 | 72.32 | 22.84 | 521.69 | 22.84 |

HICP: Furniture, Household Equipment, and Routine Household Maintenance Price Index | (2015=100) | CEIC | 104.48 | 100.99 | 6.55 | 42.92 | 6.55 |

Euro Area Harmonised Index of Consumer Prices | % | CEIC | 2.01 | 1.57 | 1.21 | 1.47 | 1.21 |

Container Throughput Index: Asia: China | (2015=100) | CEIC | 117.46 | 115.81 | 18.98 | 360.25 | 18.98 |

Container Throughput Index: Northern Europe: Baltic Sea | (2015=100) | CEIC | 122.83 | 125.41 | 14.96 | 223.79 | 14.96 |

Container Throughput Index: Northern Europe: North Sea | (2015=100) | CEIC | 106.13 | 105.45 | 7.16 | 51.27 | 7.16 |

Container Throughput Index: Southern Europe | (2015=100) | CEIC | 113.74 | 116.76 | 12.46 | 155.24 | 12.46 |

Korea Unemployment Rate | % | Organisation for Economic Co-operation and Development | 3.43 | 3.40 | 0.67 | 0.44 | 0.67 |

Korea Loan Interest Rate | Annual Interest Rate % | Bank of Korea | 3.93 | 3.66 | 0.80 | 0.64 | 0.80 |

USD/KRW | USD/KRW | Bank of Korea | 1184.13 | 1150.07 | 105.99 | 11234.27 | 105.99 |

Korea CPI | (2020=100) | Statistics Korea | 101.25 | 99.43 | 7.04 | 49.57 | 7.04 |

Korea Exports to EU | Thousand USD | Korea Customs Service | 4747721.18 | 4636431.00 | 821650.75 | 675109958136.68 | 821650.75 |

Indonesia Short-Term Lending / Interbank Money Market Interest Rate | % | Organisation for Economic Co-operation and Development | 5.32 | 5.61 | 1.56 | 2.42 | 1.56 |

Indonesian Rupiah to US Dollar | USD/IDR | Bank Indonesia | 13909.26 | 14134.50 | 1526.11 | 2329000.58 | 1526.11 |

Japan Unemployment Rate | % | Statistics Bureau of Japan | 2.91 | 2.80 | 0.52 | 0.27 | 0.52 |

Japan CPI | (2020=100) | Statistics Bureau of Japan | 100.53 | 99.70 | 3.99 | 15.88 | 3.99 |

Japan Exports to EU | Billion JPY | Ministry of Finance Japan | 705.33 | 698.14 | 114.48 | 13104.89 | 114.48 |

Japan Preferred Loan Interest Rate | Annual Interest Rate % | Bank of Japan | 1.49 | 1.48 | 0.05 | 0.00 | 0.05 |

Japan Foreign Exchange: US Dollar | USD/JPY | Mitsubishi UFJ Financial Group | 118.26 | 111.89 | 16.89 | 285.34 | 16.89 |

New Zealand Exports to EU | Million NZD | Statistics New Zealand | 334.97 | 318.01 | 91.55 | 8381.57 | 91.55 |

US Dollar to New Zealand Dollar | NZD/USD | Reserve Bank of New Zealand | 0.69 | 0.68 | 0.07 | 0.01 | 0.07 |

New Zealand Official Cash Rate | Annual Interest Rate % | Reserve Bank of New Zealand | 2.48 | 2.25 | 1.57 | 2.46 | 1.57 |

Singapore CPI | (2024=100) | Singapore Department of Statistics | 88.71 | 85.70 | 5.55 | 30.83 | 5.55 |

USD/SGD | USD/SGD | Monetary Authority of Singapore | 1.35 | 1.35 | 0.05 | 0.00 | 0.05 |

Singapore Exports to EU | Million SGD | Enterprise Singapore | 4344.64 | 4209.20 | 698.13 | 487380.72 | 698.13 |

Philippines CPI | (2012=100) | Philippine Statistics Authority | 103.71 | 102.05 | 12.86 | 165.40 | 12.86 |

Philippines Exports to EU | Million USD | International Monetary Fund | 626.62 | 625.44 | 121.73 | 14818.07 | 121.73 |

USD/PHP | USD/PHP | Bangko Sentralng Pilipinas | 50.38 | 50.66 | 4.66 | 21.71 | 4.66 |

Indonesia CPI Month-over-Month Growth Rate | % | Statistics Indonesia | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Indonesia Exports to EU | Million Dollar | Statistics Indonesia | 1679.90 | 1592.53 | 294.19 | 86550.57 | 294.19 |

EUDR | European Union Deforestation Regulation |

EU | European Union |

LASSO | Least Absolute Shrinkage and Selection Operator |

OLS | Ordinary Least Squares |

EUTR | European Union Timber Regulation |

SMEs | Small and Medium Enterprises |

CGE | Computable General Equilibrium |

HS code | Harmonized System Codes |

CPI | Consumer Price Index |

HICP | Harmonized Index of Consumer Prices |

EUDR | European Union Deforestation Regulation |

| [1] | Yin, Z. H., Li, J. Q., Tian, H., et al. (2011). Impacts of EU Timber Regulation on international trade of forest products and China's countermeasures. Research of Agricultural Modernization, 32(5), 537-541. |

| [2] | Hou, X. Y.; Yin, Z. H.; Qiu, L. Y.; et al. Study on the challenges of EU Timber Regulation to China's wood forest products trade and countermeasures. Forestry Economics 2013, 37, 54-57. |

| [3] | Hou, F. M.; Zhuang, J. Q. Impact analysis of EU Timber Regulation on China's wooden furniture exports to the EU. Journal of Xi’an University of Finance and Economics 2015, 28, 99-105. |

| [4] |

Brack, D. (2017). The European Union’s Timber Regulation: Is it working? Chatham House URL:

https://www.chathamhouse.org/2017/06/european-unions-timber-regulation-it-working |

| [5] | Mao, X. Y.; Chen, Y.; Jiang, H. F. EU's Regulation on deforestation-free products and its impacts and countermeasures. World Forestry Research 2022, 35, 93-98. |

| [6] | Simonnet, A. The impact of the European Deforestation-Free Regulation on trade relations with Southeast Asia. Regulation (EU) 2023, 1115. |

| [7] |

Permatasari, A. P.; Fauziyah, D.; Naufal, F.; Afian, S.; Nisa, S.; Fetra, T.; Hadad, N. Strengthening Indonesia’s readiness to navigate the European Union Deforestation-Free regulation through improved governance and inclusive partnership. 2024. URL:

https://madaniberkelanjutan.id/wp-content/uploads/2024/03/Madani-Update-EUDDR-ENG_Final.pdf |

| [8] | Jopke, P., & Schoneveld, G. C. (2022). The European Union Deforestation Regulation: A primer for policymakers in producer countries. CIFOR. URL: |

| [9] | Roldan Muradian, Raras Cahyafitri, Tomaso Ferrando, Carolina Grottera, Luiz Jardim-Wanderley, Torsten Krause, Nanang I. Kurniawan, Lasse Loft, Tadzkia Nurshafira, Debie Prabawati-Suwito, Diaz Prasongko, Paula A. Sanchez-Garcia, Barbara Schröter, Diana Vela-Almeida. Will the EU deforestation-free products regulation (EUDR) reduce tropical forest loss? Insights from three producer countries. Ecological Economics. 225(227): 108389. |

| [10] | Anderson, J. E. A theoretical foundation for the gravity equation. Am. Econ. Rev. 1979, 69, 106-116. |

| [11] | Larson, J.; Baker, J.; Latta, G.; Ohrel, S.; Wade, C. Modeling International Trade of Forest Products: Application of PPML to a Gravity Model of Trade. Forest Products Journal 2018, 68, 303-316. |

| [12] | Nasrullah, M.; Chang, L.; Khan, K.; Rizwanullah, M.; Zulfiqar, F.; Ishfaq, M. Determinants of forest product group trade by gravity model approach: A case study of China. Forest Policy and Economics 2020, 113, 102117. |

| [13] | Xu, Y. S.; Hou, F. M.; Shi, Z. H.; et al. Impact of EU Deforestation-free Regulation on China's forest products trade: An analysis based on GTAP model. World Forestry Research 2025, 38, 94-101. |

| [14] | Hu, Y. H.; Meng, Q.; Xia, J.; Chen, N. Impact of EU Deforestation-free Regulation on China's forest products trade. Working paper 2025. |

| [15] | Wang, F. T.; Liu, S. T.; Cheng, B. D.; Jiang, Q. E.; Tian, Y.; Xiong, L. C. How Can Intra Industry Trade of Forest Products be Promoted? An Empirical Analysis from China. Forests 2019, 10, 882. |

| [16] | Tibshirani, R. Regression shrinkage and selection via the LASSO. Journal of the Royal Statistical Society: Series B (Methodological) 1996, 58, 267-288. |

| [17] | Medeiros, M. C.; Vasconcelos, G. F.; Veiga, Á.; Zilberman, E. Forecasting inflation in a data-rich environment: the benefits of machine learning methods. Journal of Business & Economic Statistics 2021, 39, 98-119. 23. |

APA Style

Hu, Y., Meng, Q., Chen, N., Yuan, M., Xia, J. (2025). Forecasting the Impact of the EU Deforestation Regulation (EUDR) on Asia-Pacific Forest Product Trade. American Journal of Environmental and Resource Economics, 10(4), 149-160. https://doi.org/10.11648/j.ajere.20251004.14

ACS Style

Hu, Y.; Meng, Q.; Chen, N.; Yuan, M.; Xia, J. Forecasting the Impact of the EU Deforestation Regulation (EUDR) on Asia-Pacific Forest Product Trade. Am. J. Environ. Resour. Econ. 2025, 10(4), 149-160. doi: 10.11648/j.ajere.20251004.14

AMA Style

Hu Y, Meng Q, Chen N, Yuan M, Xia J. Forecasting the Impact of the EU Deforestation Regulation (EUDR) on Asia-Pacific Forest Product Trade. Am J Environ Resour Econ. 2025;10(4):149-160. doi: 10.11648/j.ajere.20251004.14

@article{10.11648/j.ajere.20251004.14,

author = {Yuanhui Hu and Qian Meng and Neng Chen and Mei Yuan and Jie Xia},

title = {Forecasting the Impact of the EU Deforestation Regulation (EUDR) on Asia-Pacific Forest Product Trade},

journal = {American Journal of Environmental and Resource Economics},

volume = {10},

number = {4},

pages = {149-160},

doi = {10.11648/j.ajere.20251004.14},

url = {https://doi.org/10.11648/j.ajere.20251004.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajere.20251004.14},

abstract = {This study provides a comprehensive, quantitative forecast of the dynamic impact of the European Union Deforestation Regulation (EUDR) on forest product exports from nine major Asia-Pacific economies to the EU market. To address the complexity of this policy shock, we develop a novel two-stage forecasting framework that integrates LASSO regression for high-dimensional variable selection with OLS modeling. This approach generates dynamic monthly projections from October 2025 to December 2027, simulating the policy’s effect by combining a historical proxy from the European Union Timber Regulation (EUTR) with a calibrated “intensity multiplier” based on the EUDR country-risk classification. Our projections reveal a distinct multi-phase adjustment process across the region: an immediate, sharp contraction in Q4 2025, followed by a period of significant volatility and supply chain disruption throughout 2026, and an uneven recovery in 2027. The findings underscore substantial heterogeneity in impacts driven by the EUDR risk-based framework. Standard-risk countries, such as Indonesia and Malaysia, are projected to face severe volatility and suppressed growth trajectories, with Malaysia’s exports showing particular vulnerability. In contrast, some smaller, low-risk nations like the Philippines may capitalize on a substitution effect, gaining market share as larger suppliers struggle with compliance. The study concludes that the EUDR acts as a powerful disruptive force, reshaping competitive dynamics and necessitating urgent policy responses, including enhanced traceability infrastructure and strategic market diversification, for Asia-Pacific exporters.},

year = {2025}

}

TY - JOUR T1 - Forecasting the Impact of the EU Deforestation Regulation (EUDR) on Asia-Pacific Forest Product Trade AU - Yuanhui Hu AU - Qian Meng AU - Neng Chen AU - Mei Yuan AU - Jie Xia Y1 - 2025/12/09 PY - 2025 N1 - https://doi.org/10.11648/j.ajere.20251004.14 DO - 10.11648/j.ajere.20251004.14 T2 - American Journal of Environmental and Resource Economics JF - American Journal of Environmental and Resource Economics JO - American Journal of Environmental and Resource Economics SP - 149 EP - 160 PB - Science Publishing Group SN - 2578-787X UR - https://doi.org/10.11648/j.ajere.20251004.14 AB - This study provides a comprehensive, quantitative forecast of the dynamic impact of the European Union Deforestation Regulation (EUDR) on forest product exports from nine major Asia-Pacific economies to the EU market. To address the complexity of this policy shock, we develop a novel two-stage forecasting framework that integrates LASSO regression for high-dimensional variable selection with OLS modeling. This approach generates dynamic monthly projections from October 2025 to December 2027, simulating the policy’s effect by combining a historical proxy from the European Union Timber Regulation (EUTR) with a calibrated “intensity multiplier” based on the EUDR country-risk classification. Our projections reveal a distinct multi-phase adjustment process across the region: an immediate, sharp contraction in Q4 2025, followed by a period of significant volatility and supply chain disruption throughout 2026, and an uneven recovery in 2027. The findings underscore substantial heterogeneity in impacts driven by the EUDR risk-based framework. Standard-risk countries, such as Indonesia and Malaysia, are projected to face severe volatility and suppressed growth trajectories, with Malaysia’s exports showing particular vulnerability. In contrast, some smaller, low-risk nations like the Philippines may capitalize on a substitution effect, gaining market share as larger suppliers struggle with compliance. The study concludes that the EUDR acts as a powerful disruptive force, reshaping competitive dynamics and necessitating urgent policy responses, including enhanced traceability infrastructure and strategic market diversification, for Asia-Pacific exporters. VL - 10 IS - 4 ER -

The Coordination Center for the Forest Networks in the Asia-Pacific, National Forestry and Grassland Administration of China, Beijing, China

Research Institute of Forestry Policy and Information, Chinese Academy of Forestry, Beijing, China

Global Green Supply Chain of Forest Products (Macao) Federation, Macao, China

The Coordination Center for the Forest Networks in the Asia-Pacific, National Forestry and Grassland Administration of China, Beijing, China

School of Economics, Central University of Finance and Economics, Beijing, China